Cold, inclement weather this past Winter, followed by war in Iran, put a damper on shopping center net absorption during Q1 2026 and consumer sentiment continued to track lower. Meanwhile, investment offerings continued to rise as private and institutional investors increasingly focused on grocery-anchored necessity-based retail opportunities, driving pricing higher.

Consumer Confidence Wanes in Face of Higher Inflation

U.S. consumer confidence ended the First Quarter at the lowest reading in the University of Michigan Consumer Sentiment Index’s 70-year history. Households remain highly cautious around discretionary spending, large purchases and financial commitments. Current conditions dropped to 50.1 in March from 55.8 in February and expectations fell to 46.1 from 51.7 over the same time period, driven mostly by the spike in inflation expectations based upon rising energy prices. The U.S. Bureau of Labor Statistics’ March 2026 headline CPI rose 3.3% year-over-year, the highest annual rate since April 2024, driven almost entirely by a 10.9% surge in energy costs. Per Ben Emons, founder of FedWatch Advisors, “The disruption of the strait is a multi-commodity supply chain shock….Combined, these commodities account for zero percent of the CPI’s direct weight, but their effective weight, which reflects their indirect impact on food, housing, medical care and goods, is more than 20%. This is where the affordability crash hits home especially hard because food, housing and medical care account for more than 75% (!) of household budgets.” Navy Federal Credit Union Senior Economist Heather Long adds, “Americans are upset about the war in Iran and they are showing it. [Consumers] have been clear that their top concern is affordability.”

Job growth was uneven during the First Quarter 2026, with a 160,000 gain in January, a 133,000 loss in February and a 178,000 gain in March, resulting in an unemployment rate of 4.3% at quarter end and wage growth at 3.5% year-over-year. Hiring remains concentrated in a handful of sectors, including health care, construction, transportation and warehousing. Job weakness was most pronounced in accommodation and food services. Professional and business services, information, retail and leisure and hospitality all were flat.

The U.S. Census Bureau released its advance estimate of retail and food services sales for February 2026 on April 1, showing total spending up 3.7% from a year earlier and 3.1% year-over-year for December – February. Online retailers posted a 7.5% annual sales gain and food services and drinking places were up 5.2% from February 2025 – a positive sign for restaurant and experiential retail operators.

Given this data and the continuing federal government job losses in Washington, D.C., it is somewhat surprising that the regional economy seems to be experiencing a rebound. According to Ian Anderson, CBRE’s senior director of research and analysis, the regional commercial real estate industry is improving. Per CBRE’s REVIVE Regional Vibrancy Index, which improved 68.7 points in February (the third consecutive monthly increase), “The data is pretty good. For a market like Washington, with so many of its challenges, I’m a little bit surprised on how well the data is showing itself.” Much of the monthly increase in the index was due to improvement in the mobility and visitation sub-composite, which surged 13.7% from the previous month, the largest February increase since 2022. This is likely due to more mild temperatures following the harsh stretch of weather impacting the region over the Winter.

Despite this positive news, a different survey implies that D.C.-area businesses and consumers are less confident than they were a few months ago, as the war in Iran and fears around artificial intelligence have added to consumers’ worries. According to American City Business Journal’s Metropolitan Consumer Sentiment Index, the metropolitan area’s consumer sentiment score for Q1 2026 fell to 92.4, down from a score of 98 at the end of Q4 2025 and a score of 106.1 at the end of Q1 2025. This marked the fourth consecutive quarter that the score declined and the third consecutive quarter that the score was below 100, the dividing line between positive and negative sentiments. According to the U.S. Bureau of Labor Statistics, the Washington, D.C. metropolitan area’s unemployment rate is the highest in the country, at 6.7%.

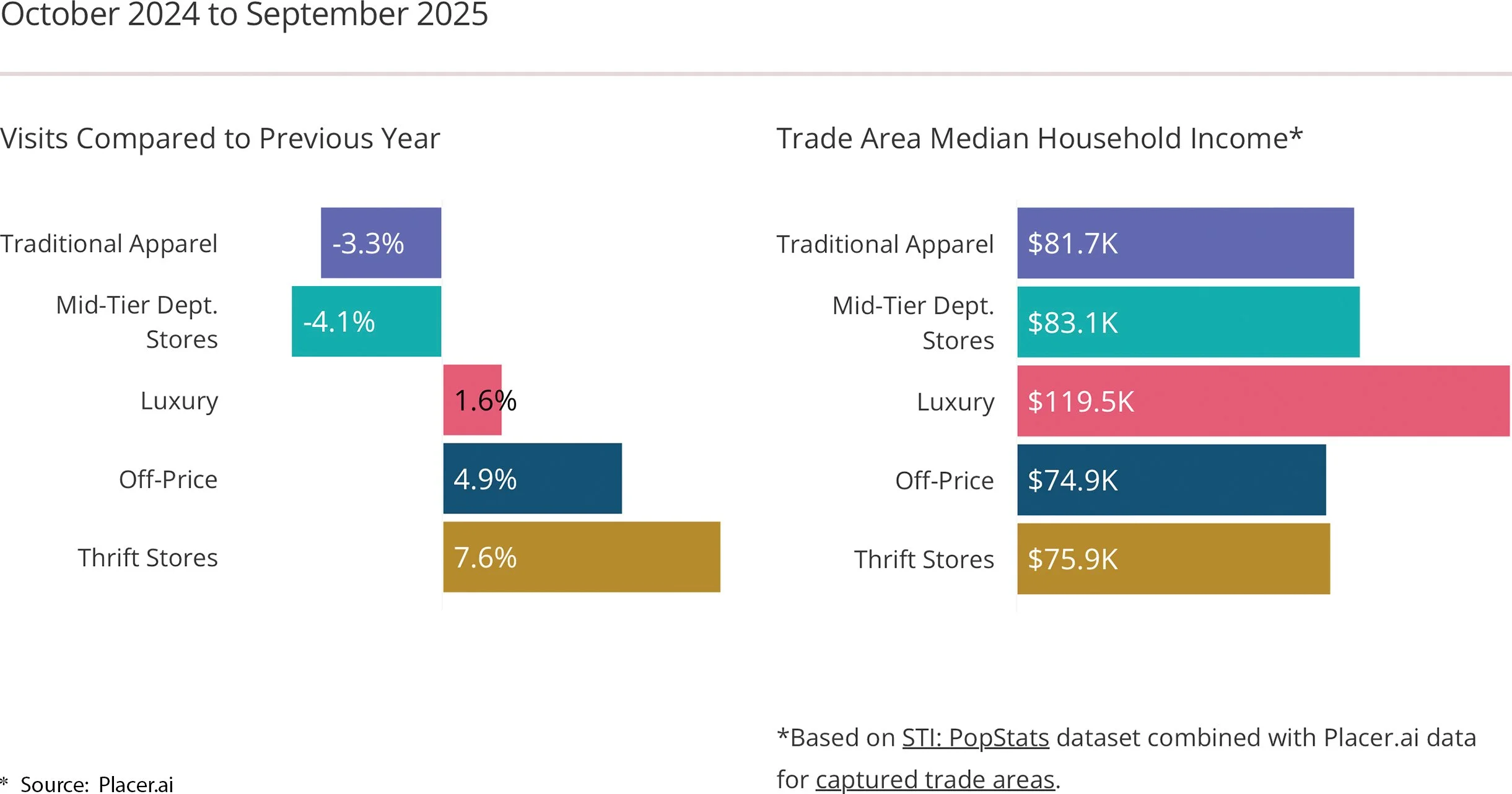

Given the economic uncertainty, off-price retailers and thrift stores continued to experience increased traffic, as consumers sought value and treasure-hunt experiences. The K-shaped economy that supported retail sales through much of 2025 continues but shows greater weakness. Luxury goods retailers continue to struggle amid increasingly constrained discretionary spending and try to regain their aspirational shopper customer base amid slower traffic and sales in mon0-brand boutiques due to rising prices. Meanwhile, traditional apparel and mid-tier department stores saw visit declines, signaling further pressure on middle-class households.

NEWS | RESEARCH

Q1 2026 White Paper

Spiking Energy Prices Cloud Optimism Regarding Brick and Mortar Retail Fundamentals

VALUE & LUXURY APPAREL VISITS GROW & MEDIAN HHI IS BIFURCATED

Upscale full-service restaurants are outperforming more casual counterparts, as diners seek elevated experiences for special occasions. More cost-conscious consumers are trading down from casual full-service restaurants to fast-casual chains. Fast-casual dining also has been benefiting from trading up within the limited-service segment, as consumers who choose to eat out opt for a premium, accessible experience.

According to Placer.ai, those retail and dining chains that are experiencing the most success in the current environment deliver an experience that feels intentional, distinctive and true to their identity. Placer.ai identifies Barnes & Noble, Trader Joe’s and Sprouts as three examples of companies that signal such authenticity and clarity of purpose. It points to H-E-B and In-N-Out Burger as regional players whose deeply-ingrained local identities have translated into sustained growth.

Although online purchases continue to grow, consumers still relate to physical locations, which are part of retailers’ omnichannel ecosystem. Convenience shopping extends to physical store visitation, as strip/convenience shopping centers outpace other formats and chains are expanding their suburban presence as work-from-home trends continue. In the grocery segment, elevated food costs are leading to more frequent, budget-conscious trips. Consumers’ desire for fresh products reinforce this trend. Shoppers are visiting multiple stores during the week with shorter visits, searching for value, availability and mission.

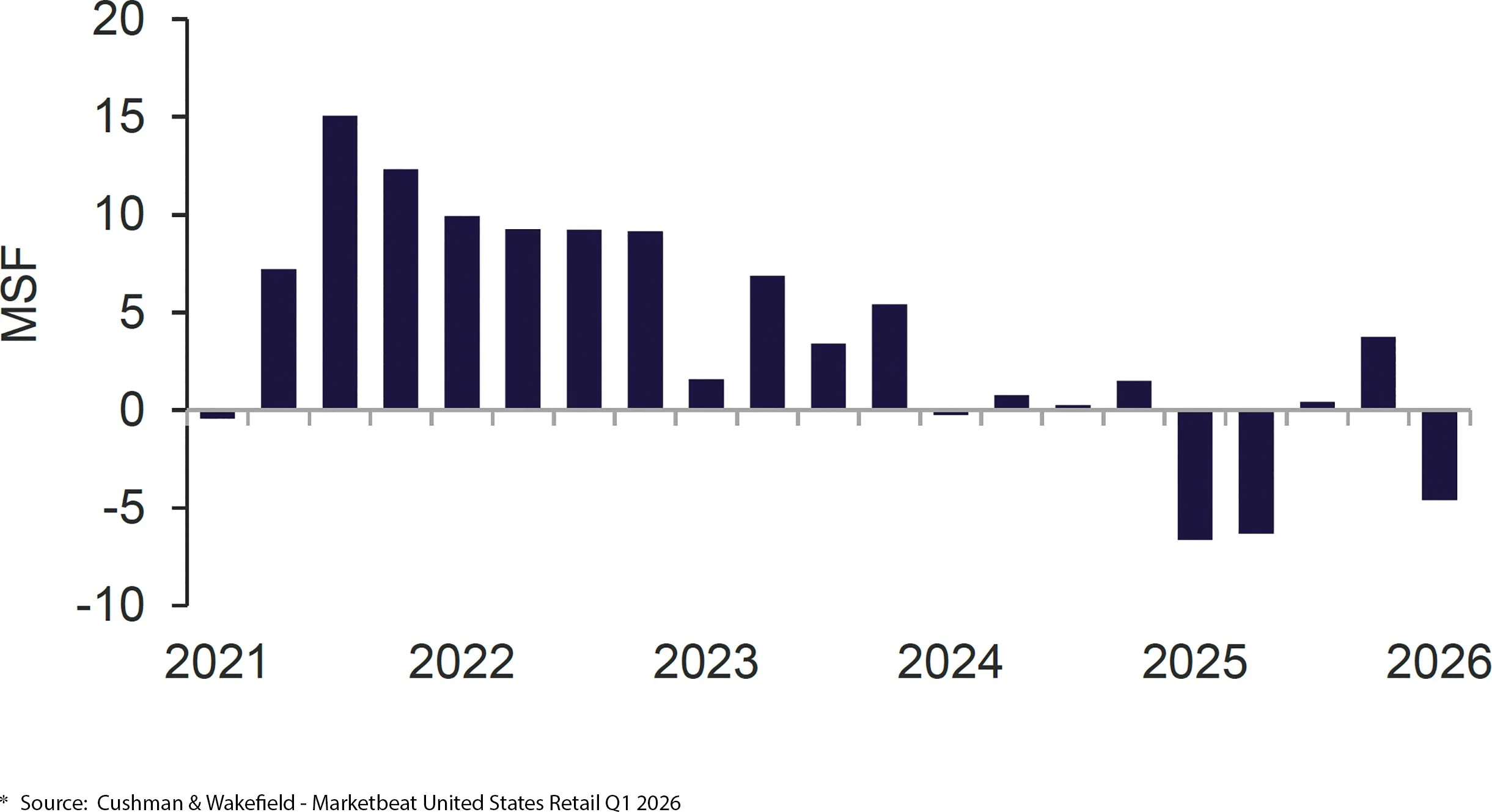

Retail Net Absorption Hit by Slow Start Due to Harsh Winter and Seasonality

After a robust Third and Fourth Quarter 2025, retail net absorption in the United States experienced negative 4.6 million square feet during the First Quarter 2026, set back by the severe Winter and planned store closures.

SHOPPING CENTER NET ABSORPTION

Leasing activity occurred amidst continued supply side constraints, as only 2.0 million square feet was delivered during Q1 2026 and 12.3 million square feet remains under construction. Significant growth in supply is not foreseeable in the near future, as already high construction prices are expected to increase further due to the energy shock and general inflation. Debt costs are not expected to decrease significantly and may increase, subject to Fed policy, the bond markets and general market uncertainty.

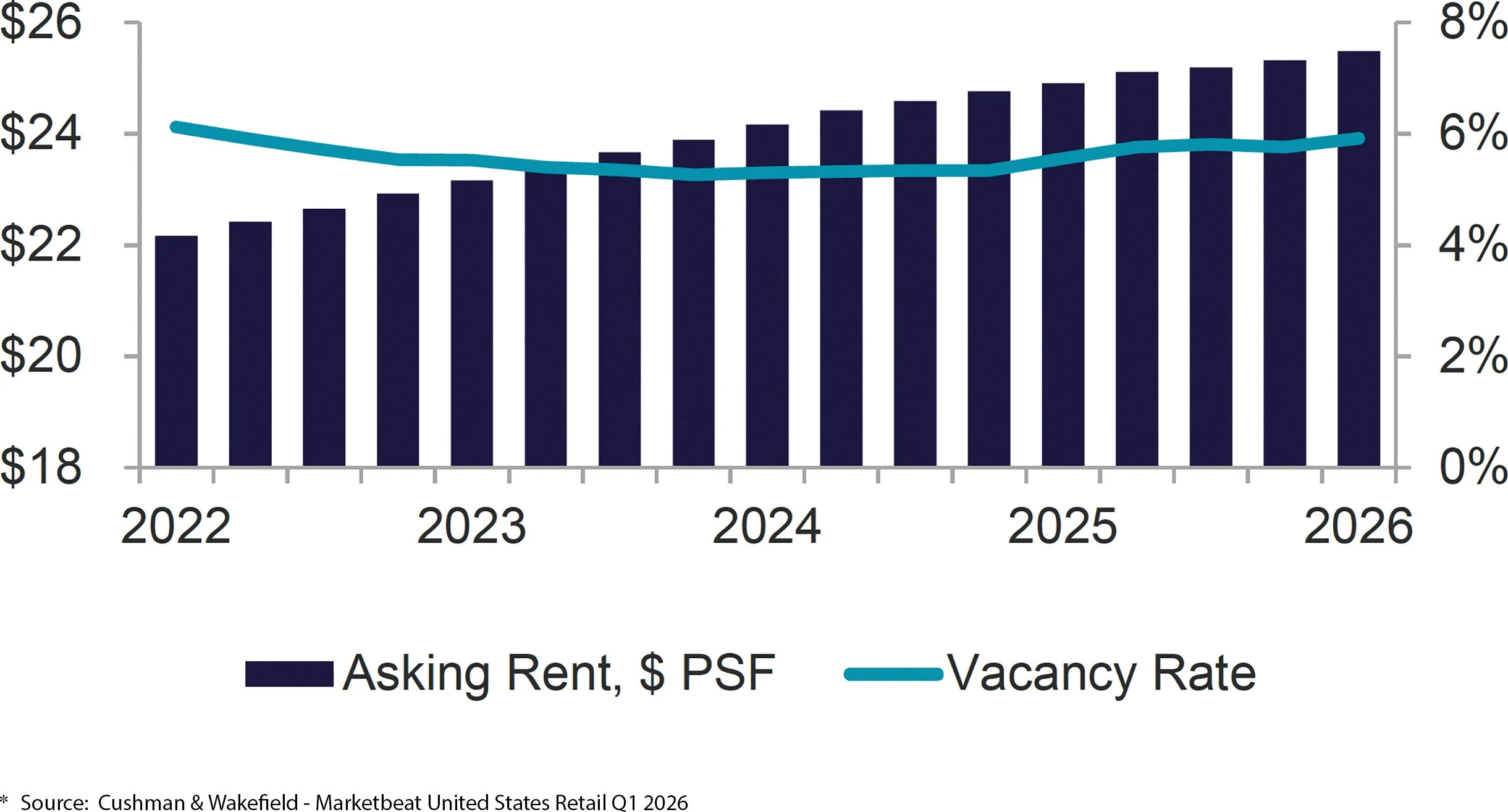

Q1 2025 vacancy ended at 5.9%, up slightly from 5.7% at the end of the Fourth Quarter. According to Cushman & Wakefield, asking rents in Q1 2026 averaged $25.48 per square foot, up from $25.29 per square foot at the end of Q4 2025. Average releasing time held steady at seven months, on average.

OVERALL VACANCY AND ASKING RENT

Washington, D.C. Metro Performs in Line with National Statistics

Based upon data presented by Cushman & Wakefield, Washington, D.C. metro area retail trends are in line with national figures. It estimates the metropolitan area open-air retail center Q1 2026 vacancy rate to be 5.1%, with asking rents of $35.60 per square foot, 221,353 square feet under construction and an in-place inventory of 119.9 million square feet. Cushman & Wakefield reports -480,883 square feet of net absorption for Q1 2026 for open-air retail in the Washington, D.C. metropolitan area.

Retail Investment Maintains Its Footing

U.S. retail investment sales and debt markets remained relatively stable, with volume and pricing increases relative to the second half of 2025. According to Cushman & Wakefield, individual asset sales are up 20% year-over-year and cap rates are stabilizing. The NCREIF Property Index has posted four consecutive quarters of positive total returns, with retail outperforming other major property types over the trailing year. Interest is being generated by retail fundamentals, including:

Relative pricing and yield premium: Retail offers attractive entry yields relative to other property types.

Limited new supply: Retail construction starts are at multi-decade lows with vacancy rates at record lows.

Tenant mix evolution: Cotenancy includes soft goods, experiential concepts, food and beverage, health and wellness and entertainment, driving traffic throughout the day and week.

Inflation-hedge characteristics: Lease contractual escalations and percentage rent clauses provide income growth tied to sales performance and inflation.

Diversification and macro tailwinds: Investors are rebalancing their portfolios after years of focus on multi-family and industrial/logistics. Retail offers diversification across cash flow duration, tenant credit and consumer-driven demand.

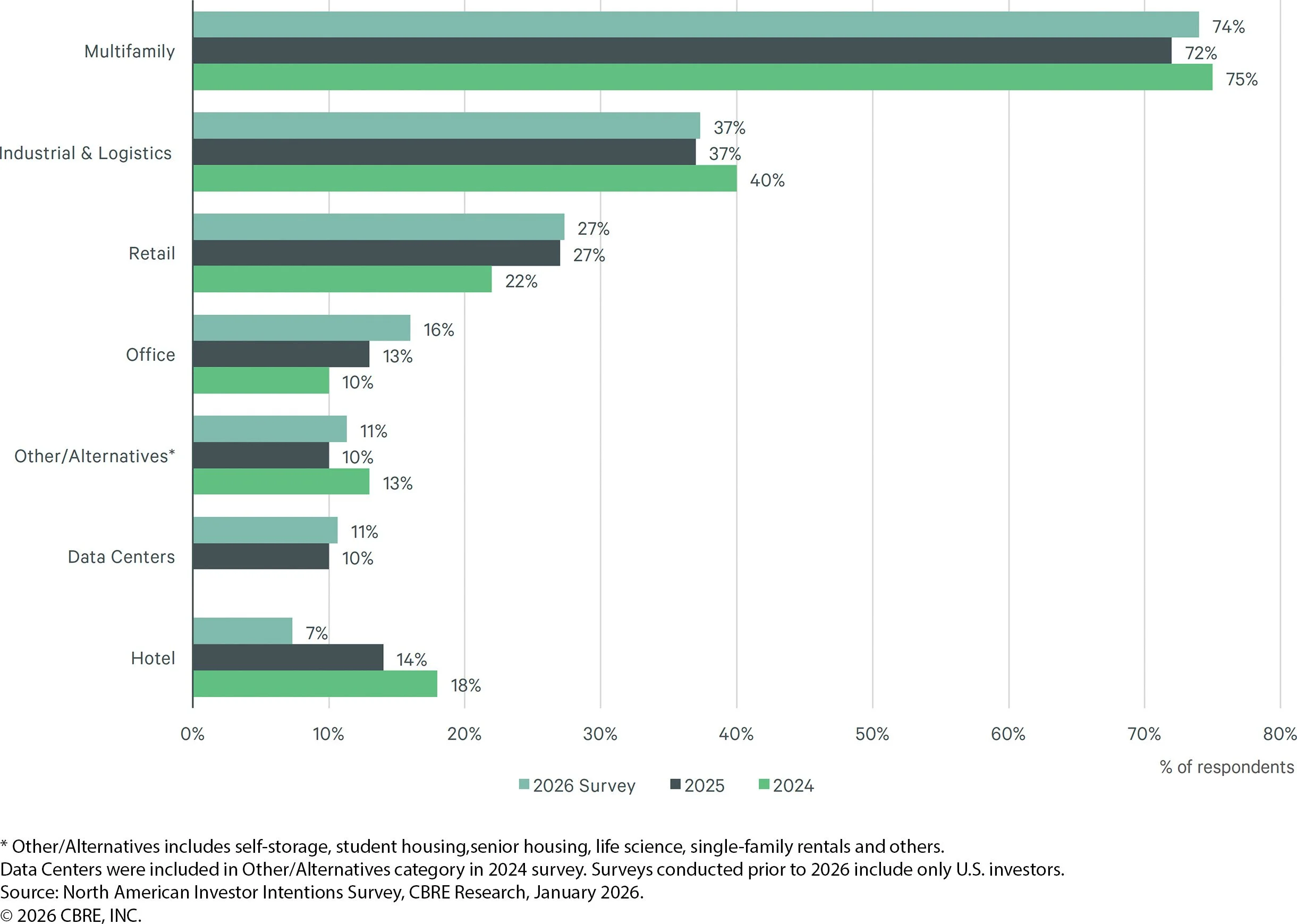

According to CBRE’s 2026 North American Investor Intentions Survey, roughly one-third of investors plan to pursue both value-add and core-plus strategies in the coming year, with 17% looking for opportunistic returns. The ranking of core-plus increased from 28% in 2025 to 32% in 2026, reflecting a shifting preference for opportunities that prioritize income-driven returns alongside a balanced risk-return profile. Investors ranked retail as its third-highest preference, behind multi-family and industrial/logistics, in line with the results of the 2025 survey. Grocery-anchored centers remained the top choice for retail investors, followed by lifestyle centers and unanchored strips, with the latter two categories pricing more readily at value-add/opportunistic return levels.

PROPERTY SECTORS TARGETED BY U.S. INVESTORS IN 2026 (MULTIPLE CHOICE)

According to the CBRE survey, nearly three-quarters of investors continue to favor direct real estate or wholly-owned real estate assets.

Portfolio-driven strategies continue to be popular. Of note was the Sterling Organization’s sale of seven shopping centers located in California, Texas, Florida and Minnesota for $298 million. Also, on behalf of a client, JLL sold seven shopping centers located in Georgia, South Carolina, Virginia and New Jersey to Medipower for $115 million. According to JLL’s Jim Hamilton, “the [portfolio] generated significant investor interest, reflecting the continued robust flow of capital into the retail sector. The strong market response underscores investor confidence in grocery-anchored retail as a resilient asset class.”

Debt financing continues to become more available to retail commercial real estate. High profile transactions included Blackstone securing a $2.8 billion CMBS financing backed by 85 grocery-anchored centers and Bridge33 completing a $460 million CMBS refinancing backed by 12 retail assets across nine states.

The Washington, D.C. metropolitan area in particular has seen a significant increase in retail shopping center sales volumes and more aggressive pricing. According to Altus Group Research, the D.C. area saw prices increase by 27% between 2024 and 2025, compared to a 12.3% increase nationally. Brokers attribute the spike to a flood of new investors competing for limited grocery-anchored product. According to Wright Sigmund, managing principal of the Sigmund Cos., “There’s more people coming in who haven’t done it in the last decade. And it’s noticeable. It’s real. It’s not just a theory.” According to CBRE First Vice President Casey Smith, several market participants see current market conditions as an opportune time to sell. She notes, “Once 2025 hit and there was a little bit more stability, everyone was ready to sell.” This has been evident by the listings sponsored by Federal Realty Investment Trust, Edens and Willard Retail, among others. Core and core-plus capital in particular has become more active after being on the sidelines for the past few years. Institutional investors and private capital that had been focused on multi-family and logistics in recent years have turned their attention to retail, pushing cap rates below 7.0% and even 6.0%. According to Smith, “Private capital has been the dominant player for the last few years and continues to be, but they’re now competing with these core groups, and that also drives pricing, because they can be very aggressive, core capital, so that’s also pushing pricing.” Some industry players are taking a closer look at unanchored retail, as the competition for grocery-anchored properties becomes too fierce.

Not all news is positive, however. The Real Estate Roundtable’s Sentiment Index for the First Quarter 2026 registered an overall score of 67, down one point from the prior quarter, as respondents described a market in the early stages of a tentative, uneven recovery. According to connectcre, interest rate uncertainty continues to widen buyer-seller spreads and slow price discovery. Moreover, CMBS delinquency rates continue to move higher. According to Trepp CMBS Research, CMBS delinquency ended the First Quarter 2026 at 7.55%, up from 7.30% at year end. Four of the five major property types saw increases in delinquencies, led by lodging.

Given its opportunistic/value add focus, SageTrust Properties approaches the current environment cautiously, but continues to be in the market to source retail open-air property acquisition opportunities and has the capability to manage its assets. Let us know if you would like to schedule a meeting with us to discuss your needs and our capabilities further.